Foreign employment changes many lives. Thousands of Nepalese go abroad with one dream: earn money, support family, clear loans, build a house, educate children, and create a better future.

But one painful reality is this: many foreign employment workers spend years abroad, earn salary every month, send money home, fulfill responsibilities, but still return with very little saving or financial security.

The problem is not always low income. Many times, the real problem is lack of financial discipline.

This is where SIP can become useful.

SIP is not a magic investment. It is not a shortcut to become rich quickly. But for foreign employment workers who want to build a saving and investment habit, SIP can be a practical and disciplined starting point.

What Is SIP?

SIP stands for Systematic Investment Plan.

In simple words, SIP is a method of investing a fixed amount regularly, usually every month, into a mutual fund or similar investment scheme.

Instead of investing a large amount at once, SIP allows you to invest small amounts consistently over time. NIC Asia Capital describes SIP as a structured way to invest small, regular amounts into mutual funds, while Nabil Invest highlights SIP benefits such as affordability, flexibility, and financial discipline.

For example, instead of thinking, “I will invest only when I have NPR 1 lakh,” you can start with a smaller regular amount every month, depending on the scheme and your capacity.

The main idea of SIP is simple:

Small amount. Regular investment. Long-term discipline.

Why SIP Is Important for Foreign Employment Workers

Foreign employment workers usually have regular monthly income. But salary alone does not create financial growth.

What matters is what you do after salary comes.

Many workers follow this cycle:

Salary comes.

Money is sent home.

Some expenses are paid.

Some money is spent personally.

Then the month ends.

Again, they wait for the next salary.

If this cycle continues for years without saving or investment habit, life may not change much even after working abroad for a long time.

SIP can help break this cycle because it encourages regular investment before money gets spent.

The Biggest Problem: “I Will Save What Is Left”

Many people say:

“I will save after expenses.”

But in reality, expenses rarely end.

Family needs continue. Personal expenses continue. Emergencies come. Festivals come. Travel costs come. Mobile phones, gifts, loans, and social pressure also come.

That is why “I will save what is left” often becomes “nothing is left.”

SIP encourages a different mindset:

Save and invest first, then spend what remains.

For foreign employment workers, this mindset is very powerful.

SIP Builds Financial Discipline

The biggest benefit of SIP is not only investment return. The biggest benefit is discipline.

When you invest a fixed amount every month, you slowly build a habit. That habit can become more valuable than the amount itself.

A person who starts with a small monthly amount but continues for years may build a stronger financial base than someone who earns more but saves nothing.

SIP helps foreign employment workers:

Create regular saving habit

Avoid unnecessary spending

Build investment discipline

Think long-term

Connect salary with future planning

Reduce dependency on emotional spending

This is why SIP is not only an investment product. It is a financial behavior.

SIP Is Light on the Wallet

Many foreign employment workers feel that investment requires a big amount. That is not always true.

One of the key features of SIP is that you can start with a small regular amount, depending on the available scheme. Nabil Invest mentions SIP as affordable and “light on your wallet,” while its SIP page lists a minimum investment example of Rs. 1,000 for its specific SIP product.

For workers abroad, this matters because not everyone can invest a big amount at once. But many can manage a small fixed amount every month if they plan properly.

The goal is not to start big.

The goal is to start consistently.

SIP Helps Manage Risk Better Than Lump Sum Investment

Investing a large amount at one time can feel risky, especially for beginners.

SIP allows you to invest gradually. Because you invest regularly over time, you do not put all your money into the market at once.

This can help manage market ups and downs through a concept often called rupee cost averaging. Siddhartha Capital explains that with SIP, investors may buy more units when the market is low and fewer units when the market is high, which can help average the cost over time.

However, this does not mean SIP removes risk completely.

It only helps you invest in a more disciplined and gradual way.

SIP Is Not Guaranteed Profit

This is very important.

SIP is not guaranteed profit.

Mutual fund investments are subject to market risk. Siddhartha Capital clearly mentions that mutual funds do not have a fixed rate of return and that returns cannot be predicted with certainty.

Foreign employment workers should understand this clearly before starting SIP.

SIP can help build habit and long-term discipline, but the value of investment can go up or down depending on market conditions and fund performance.

So, do not start SIP thinking it is guaranteed income.

Start SIP because you want financial discipline, long-term planning, and a systematic investment habit.

Why SIP Is Better Than Random Saving for Many Workers

Random saving depends on mood.

SIP depends on system.

Many people save only when they remember. Some save when they have extra money. Some save for two months and then stop.

SIP helps create structure.

It gives your salary a purpose.

Every month, part of your income goes toward future planning. This makes your financial life more organized.

For foreign employment workers, this is very important because income abroad often comes with pressure from many sides.

Without a system, money can disappear quickly.

SIP and Foreign Employment Income

Foreign employment income is hard-earned money.

It comes from long working hours, physical effort, homesickness, pressure, and sacrifice. Many workers live away from family for years.

That money should not only go toward daily expenses.

It should also create a future.

SIP helps foreign employment workers turn salary into a system.

Salary should not only be:

Earned

Sent

Spent

Forgotten

It should also be:

Saved

Invested

Recorded

Planned

Grown over time

This is why SIP can be especially useful for workers living abroad.

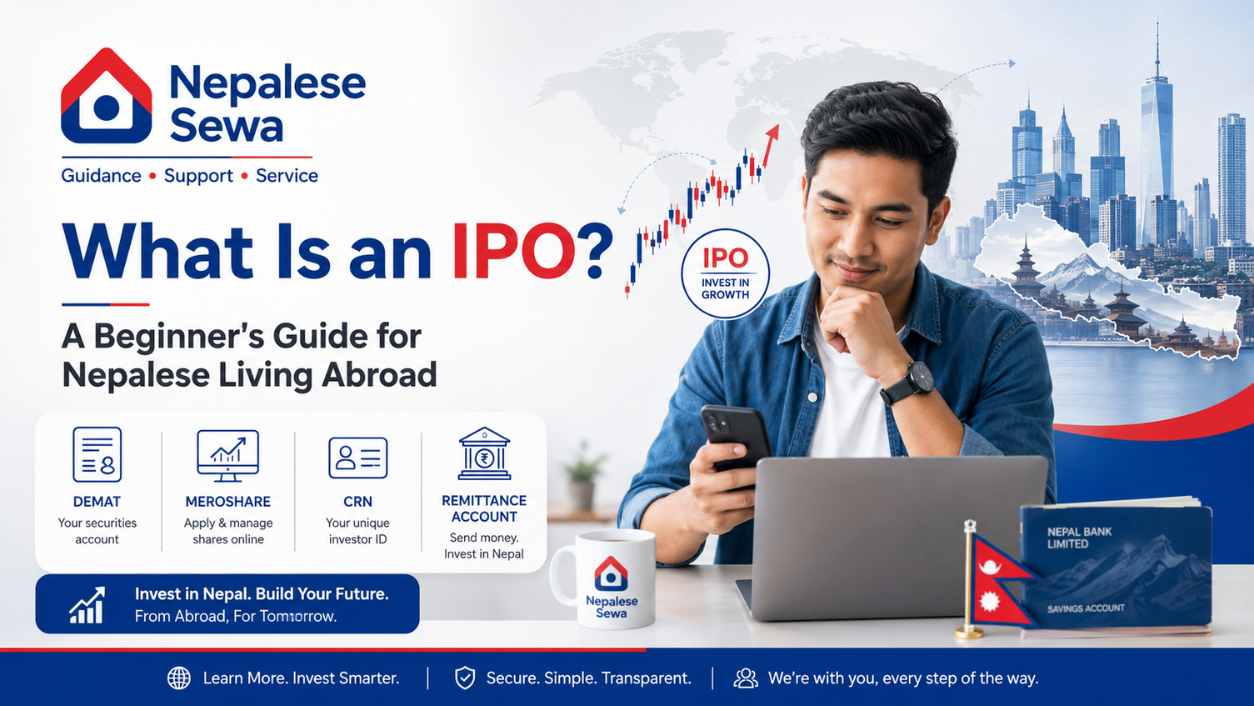

SIP vs IPO: What Is the Difference?

SIP and IPO are different investment concepts. IPO means a company offers its shares to the public for the first time, while SIP is a system of investing a fixed amount regularly over time. For Nepalese living abroad, both IPO and SIP can be important parts of financial awareness and long-term planning.

If you want to understand IPO from a beginner level, you can read our detailed article on IPO in Nepal for Nepalese Living Abroad, where we explain IPO, Demat Account, MeroShare, CRN Number, Remittance Account, and the basic process of applying for IPO in Nepal.

Many Nepalese abroad are interested in IPO. An IPO can be a good way to start understanding shares and investment.

But IPO and SIP are different.

IPO means applying for shares when a company offers them to the public for the first time.

SIP means investing a fixed amount regularly into a mutual fund or investment scheme.

IPO depends on allotment. You may get shares or you may not.

SIP is more about regular habit. You invest consistently over time.

For foreign employment workers, both IPO and SIP can be part of financial awareness. But SIP is especially useful for building long-term discipline.

SIP and Emergency Fund: Which Comes First?

Before investing aggressively, every foreign employment worker should also think about emergency fund.

Emergency fund means money kept separately for unexpected situations like:

Job loss

Medical emergency

Family emergency

Travel emergency

Visa-related issue

Urgent home need

SIP is important, but emergency fund is also important.

A practical approach is to think about saving, emergency fund, and investment together.

You do not need to wait many years to start investing. But you should not invest all your money without keeping emergency backup either.

Balance is important.

Common Mistakes Foreign Employment Workers Make

Many foreign employment workers make these mistakes:

They send money home without tracking where it goes.

They wait for “big money” before starting investment.

They spend first and try to save later.

They invest only because someone else said so.

They stop saving when family expenses increase.

They do not keep emergency fund.

They do not understand risk.

They expect guaranteed profit.

They do not review their financial plan.

SIP can help reduce some of these mistakes by creating a regular investment habit.

But SIP should be done with proper understanding.

Who Should Consider SIP?

SIP may be useful for foreign employment workers who:

Have monthly income

Want to build saving habit

Cannot invest a large amount at once

Want long-term financial planning

Want to start investment slowly

Want to reduce unnecessary spending

Want to prepare for future goals

Want to build discipline

SIP may not be suitable if you are expecting quick profit, guaranteed return, or short-term money doubling.

It is better for people who can stay consistent.

How Much Should Foreign Employment Workers Start With?

There is no one answer for everyone.

It depends on your salary, family responsibility, loan, living cost, emergency fund, and financial goal.

But the best rule is:

Start with an amount you can continue.

Do not start too big and stop after two months.

It is better to start small and continue for a long time.

For example, if you can regularly set aside a small amount every month without disturbing your basic needs, that can be a good beginning.

Consistency matters more than showing off a big amount.

Why Family Should Also Understand SIP

Many foreign employment workers send money to family in Nepal.

But if the family does not understand financial planning, the money may be spent without long-term benefit.

That is why financial awareness should not only be for the person abroad. Family members in Nepal should also understand:

Why saving is important

Why every remittance should not be fully spent

Why investment planning matters

Why emergency fund is necessary

Why records should be maintained

Why long-term discipline matters

SIP can become a family financial planning tool if both the worker abroad and family in Nepal understand the purpose.

SIP Is Not Only About Money

SIP is about mindset.

It teaches you:

Patience

Consistency

Discipline

Planning

Long-term thinking

Control over spending

For foreign employment workers, this mindset is very important.

Because abroad life can become a cycle:

Work

Earn

Send

Spend

Repeat

SIP helps add one more important step:

Build.

Work. Earn. Send. Spend. But also build.

How Nepalese Sewa Can Help

Nepalese Sewa helps Nepalese in Nepal and abroad with documentation, financial readiness, and guidance-related services.

For foreign employment workers who want to understand SIP, Nepalese Sewa can help with:

SIP awareness

Basic investment guidance

Demat and MeroShare support

Remittance Account guidance

IPO readiness

Financial discipline awareness

Step-by-step process support

Our goal is not to promise profit.

Our goal is to help Nepalese abroad understand the process, avoid confusion, and start their financial journey with clarity.

Important Disclaimer

SIP is an investment method and is subject to market risk.

Nepalese Sewa does not guarantee profit, fixed return, or investment success.

Investment decisions should be made after understanding your financial situation, risk level, and long-term goals.

This article is for educational and awareness purposes only.

Final Thoughts

Foreign employment is not easy.

Every dirham, riyal, ringgit, won, yen, dollar, or other foreign currency earned by Nepalese workers comes with hard work and sacrifice.

That money should not disappear without direction.

SIP can help foreign employment workers build discipline, start small, invest regularly, and think long-term.

You do not need to be rich to start planning.

You need discipline.

If you are living abroad and want to turn your income into future planning, start learning about SIP today.

If you are confused about how to start SIP, Demat, MeroShare, IPO, or financial readiness process, Nepalese Sewa is here to guide you.

Nepalese Sewa

Guidance • Support • Service